A Crop Insurance Scheme

The Finance Minister Mr Arun Jailtley introduced Pradhan Mantri Fasal Bima Yojana. He introduced the scheme in the Union Budget 2016 – 17. Subsequently he allocated a budget of Rs 1, 240 crores. Later the amount was raised to Rs 5, 500 crores.

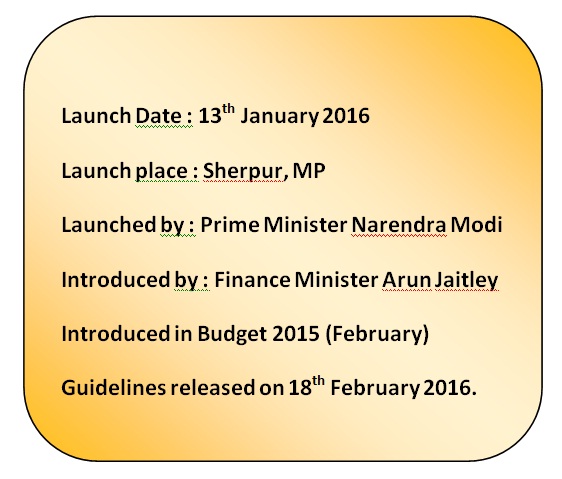

Soon on 13th January 2016, the Prime Minister Narendra Modi officially launched Pradhan Mantri Fasal Bima Yojana.

Guidellines of PMFBY

On 18th February 2016, Prime minister Narendra Modi released the operating guidelines of Pradhan Mantri Fasal Bima Yojana. And, he introduced the scheme in Sherpur village, MP

In the second place, You can download the guidelines in PDF format here.

Objectives of PMFBY

- As a rule, the scheme provides financial support to crop loss / damages. Particularly, to the unforeseen events.

- Above all, PMFBY encourages farmers to adopt innovative and modern agricultural practices.

- Lastly, the scheme ensures

- Food Security

- Crop Diversification

- Enhanced growth in agricultural sector

Coverage of Crops

The crops covered under the scheme are Rabi, Kharif and other commercial and horticultural crops. In brief, the following crops are eligible

- Food Crops (Cereals, Pulses and millets)

- Oilseeds

- Commercial and Horticultural crops

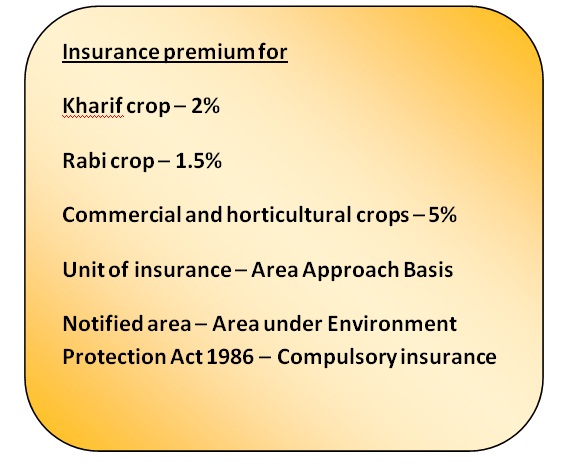

Furthermore, the Kharif crops gets a premium of 2 % whereas the Rabi crops gets only 1.5 %. Subsequently, the commercial and horticultural crops gain a premium of 5%.

Inclusions and Exclusions of PMFBY

- Inclusions

Pradhan Mantri Fasal Bima Yojana insures standing crops on notified area basis. Also, the scheme provides compensations to non – preventable risks like

- Cyclone, Typhoon, Hurricane, in brief natural storms

- Drought and dry spells

- Pests

- NAtural fire

- Flood, Landslide and lastly Lightning

2. Prevented sowing

Suppose the farmer intends to sow or plant his insured crop. Later due to adverse weather conditions he is unable to do so. He shall now be eligible for an indemnity of 25% of his losses.

3. Post – Harvest Losses

Following the harvest, the insurance coverage is available for 14 days. Provided the plants are cut and spread. More over, the insurance can be claimed only under the included circumstances.

4. Exclusions

On the contrary, PMFBY is not applicable to the following circumstances

- War

- Riots, theft and act of enemity

- Nuclear risks

- Destroyed by domestic or wild animals

- Maliciuos damage

Unit of Insurance

“Area Approach Basis” is the key factor of PMFBY. An affected farmer can claim his insurance based on the conditions of his environmental area. In other words, the above said inclusion factors are considered.

The Unit of Insurance is Village or Village Panchayat for major crops. On the other hand, the unit is at a higher level for minor crops.

Compulsory coverage – Notified area and crops

For a notified crop in the notified area, the scheme immediately comes into action. The government makes it compulsory for the following categories of farmers

- Farmers in the notified area with a crop Loan Account can avail the scheme sooner. These farmers are the “Loanee Farmers”.

- Furthermore the government sanctions or renews the credit limit for the notified crop immediately. Eventually this happens in the particular crop season.

In short a notified crop in a notified area gets a complete coverage.

What is a notified area or a notified crop?

The area or a crop that comes under Environment Protection Act 1986 is called a notified area. In such areas underground water is not permissible for any purpose other than domestic uses.

Previous Crop Insurance Schemes

Pradhan Mantri Fasal Bima Yojana mainly replaces the two existing schemes namely NAIS and the modified NAIS – National Agricultural Insurance Scheme.

Beside NAIS the other schemes are

- 1985 – Comprehensive Crop Insurance Scheme

- 1999 – NAIS

- 2007 – Weather Based Crop Insurance Scheme

- 2010 – MNAIS – Modified NAIS

PMFBY and Budget 2017

According to the Budget 2017 report presented by the Finance Minister, the PMFBY is to get an upraisal. In other words, the coverage of the scheme will be increased to 40%. Earlier, it was 30%. Furthermore it will be raised to 50% in the future according to Mr Jailtley.

Having said earlier, the amount allocated to the PMFBY in 2016-17 was Rs 5, 500 crores; it is now increased to Rs 13, 240 crores.

Analysis of PMFBY

Increased Financial burden on Government

The most benefitting factor of the scheme is its low premium. As said before 1.5%, 2% and 5% are the premium rates.

However, this will increase the financial burden on the government. The scenario specifically arises as the government indends to contribute five times the premium paid by the farmer.

Comparing PMFBY internationally

The rate of subsidy in crop premiums is not out of line when compared internationally. For example, the United States insures its farmers with a subsidy of 70%. In the same way China insures for 80%. On the other hand India has just insured 50%. Hence,

Challenges of PMFBY

- Farmers view insurance as an investment. Launch of compulsory crop insurance is a good step. In other words, the Government provides a default option of insurance along with loans.

- A transparent assessment of crop damage is missing. The compensations has to reach farmers within a specified short time of weather shocks.

- Lastly, the share of subsidy between the state and the centre is definitely the biggest challenge. For instance, the state and the centre might assess seperately. In such cases, issues arise when the assessments do not match.

The WTO norms

WTO – World Trade Organization.

WTO fixes a 30% threshold. It says that the farmer’s annual income should be less than his preceding five years. Also, in order to claim the insurance, his income loss should be less than 30% of his 5 year income.

Anti – arguments of PMFBY

- The scheme by itself does not address the biggest problem. That is the FARMER’s POOR INCOMES. About 70% of the farmers are operating on less than a hectare. Also, they are earning much less than their minimum expenditure. According to the Socio – Economic Caste Census 2011, the per capita of 75% of the rural household is less than Rs 5, 000. With such a low income, it is almost impossible to sustain the actuarial premium rates of PMFBY.

- A very few farmers actually insure their crops. (Source NSSO report)

- For instance, 95.2% of paddy farmers insures in 2012. Whereas 96.1% of them did not insure in the consecutive year of 2013.

- Likewise, 95.3% of the wheat farmers insured in 2012. Whereas 95.9% of them did not insure in 2013.

Quiz on PMFBY – Test yourself

- When was Pradhan Mantri Fasal Bima Yojana launched?

- Who introduced the scheme?

- What two schemes were replaced by PMFBY?

- What is the insurance premium percentage for a Kharif crop?

- Did Budget 2017-18 allocate an amount to PMFBY?

- Is PMFBY contradicting WTO norms?

- Is nuclear explosion included in the scheme?

- Does the scheme provide special concerns for a notified area?

- Where was the scheme introduced first?

References: