Cheque and Demand Drafts both are used for the purpose of payments. Since it is not always possible to give the money in cash to another person or party, they are popular for doing the payments. Since the banks are involved in between the payment process, the currency paid is considered to be authentic.

![]()

A cheque is a negotiable instrument drawn on a specified banker and not expressed to be payable otherwise than on demand and cheque also includes the electronic image of a truncated cheque and a cheque in the electronic form.

- ‘a cheque in the electronic form‘ means a cheque which contains the exact mirror image of a paper cheque, and is generated, written and signed in a secure system ensuring the minimum safety standards with the use of digital signature and asymmetric crypto system.

- ‘a truncated cheque‘ means a cheque which is truncated during the course of a clearing cycle, either by the clearing house or by the bank whether paying or receiving payment. After the generation of an electronic image for transmission, the image substitutes the physical movement of the cheque in writing.

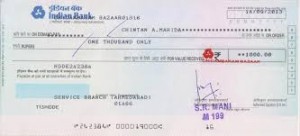

An example of cheque:

![]()

Also known as DD, it is kind of a pre-paid negotiable instrument that is used to direct payments from one bank to another bank or one of its own branches to pay a certain sum to the specified party.

- When a bank gets request for the issue of a DD by any individual or party, it either deducts the money from the bank account (if the individual/party has bank account in that bank) or individual/party has to give the amount in cash not exceeding Rs 50,000. In case of amount exceeding Rs 50,000, the payment is to be made by cheque along with giving the PAN No.

- Like a cheque, DD also contains DD number and MICR No. at the bottom. DDs can also be used for making payments abroad by issuing a draft in foreign currency.

An example of DD:

Both can be compared in many ways:

Cheque | Demand Draft (DD) |

| It is issued by an individual | It is issued by a bank |

| So they are orders of payment from an account holder to the bank | They are orders of payment by a bank to another bank |

| Payment is made after presenting cheque for encashing | Payment is paid before presenting DD for encashing |

| Three parties are involved – Drawer, Drawee, Payee | Two parties are involved – Drawer, Payee |

| Drawer and Drawee are different persons, can be same also if cheque is drawn on self | Drawer and Drawee are same bank with different branches |

| Drawer is customer of the bank | Drawer is the bank itself |

| In case of insufficient balance in the account, it can be dishonoured | It cannot be dishonoured because payment is already done for it |

| They can be paid to either bearer (who presents the cheque to bank) or order (whose name is specified on the cheque) | They are always payable to the specified party |

| It is defined in the Negotiable Instrument Act, 1881 | Although a type of negotiable instrument only, it is not defined in the act. |

| It requires a sign of individual/party | It requires a sign of banking authority and stamp of bank |

| There are no bank charges to issue a cheque | Different banks can charge differently for the issue of DD. |

| Individual/Party issuing cheque muct have a savings or current account in the bank | Individual/Party getting issued a DD may not necessarily have bank account in the bank |

")